Roth or Traditional - How to decide

The difference is marginal and that is the big difference.

USEFUL TIPSDIFFERENT PERSPECTIVE

Bert

10/10/20234 min read

Why is it that so few people understand the difference between Roth and traditional IRAs? Lots of people say that they do but I rarely see anyone getting the most important factor right. Disclosure – I am not any sort of a certified financial advisor, but I am an engineer which I think is sometimes better. In my (maybe not so) humble opinion, the important thing to evaluate is NOT tax bracket, sometimes called marginal tax rate. It is your average tax rate.

What is the difference between your tax bracket and average tax rate? The tax bracket is how much additional tax you pay on each additional dollar you earn. Hence, marginal. If you are in the 22% tax bracket and get a $1,000 raise, you will pay an additional $220 in taxes. In the US, the higher your income, the higher your tax bracket.

The average tax rate is based on the total taxes you pay for your total income while the tax rate is based on your adjusted gross income, or AGI. That detail is important. Because of the personal deduction, your income is always greater than your AGI (ignoring any weird circumstance where somehow it isn’t). Imagine the case of a flat tax rate of 10%, $100,000 income, and $20,000 personal deduction. Your tax rate is 10% but because of the personal deduction, you only pay that on $80,000, yielding $8,000 in taxes. Your average tax rate is $8,000 / $100,000 = 8%. When a progressive tax rate is in place, the difference becomes bigger. Additionally, if you have significant deductions, (mortgage interest, children, donations, etc) the difference is further increased because of larger deductions.

One reason why I think this critical difference is so often missed pertains to how Roth’s were marketed when they came out. They would assume a person invested $2,000 year into one or the other. At retirement, you have the same amount in each account but for the Roth you don’t have to pay taxes and on the traditional you do. See how great it is! Except there is a huge finger someone put on the scale. They ignore the fact that when you put $2000 into a Roth account, it cost you more by whatever your tax rate is. If it was 10%, it cost you $2,200. If you paid state taxes, it cost more. If you are self-employed, it cost even more because of social security taxes. To get closer to an apples to apples comparison, you should assume $2,200 (or more, depending) is put into the traditional account vs $2,000 into the Roth.

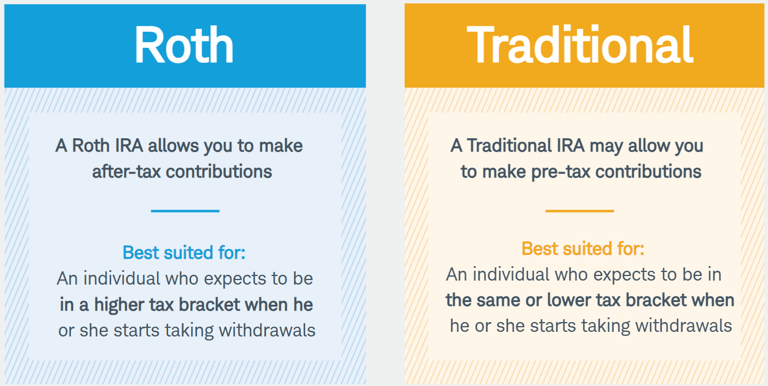

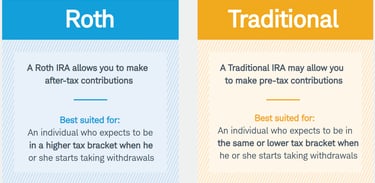

You may have asked earlier, who says to consider tax bracket? I have harped on this for years and rarely seen the difference considered properly. As an example of how pervasive the wrong thinking is, I searched for “roth vs traditional IRA comparison”. The first link on Bing was for Schwab.com. Here is a screenshot:

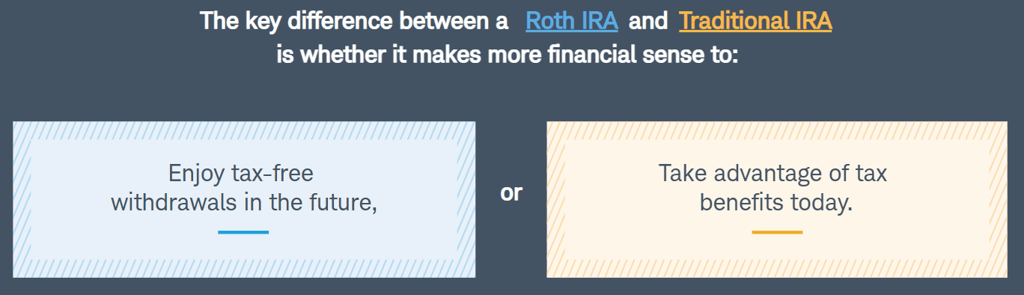

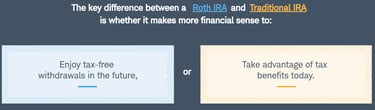

They are saying it is mostly about tax bracket and implying average tax rate is not significant. What Schwab should have written:

Roth is best suited for an individual who expects their average tax rate during retirement to be higher than their marginal tax rate today.

Traditional is best suited for an individual who expects their average tax rate for withdrawals to be lower than their marginal tax rate today.

In Schwab’s defense, there are other factors in determining Roth or traditional, but here is their summary graphic.

Those specific points may matter in some cases but most people care about having more money to live on in retirement after paying taxes. For simplicity, assume I was always in a 10% tax bracket. The appropriate comparison for a $2,000 annual deposit into a Roth is a $2,200 deposit into a traditional. Assume at retirement, the Roth IRA lets me have $50,000 a year tax free when I retire. Then, before taxes, the traditional IRA lets me have 10% more because I was putting in 10% more each year, or $55,000 a year. Currently, for a married couple filing jointly, the taxes on that would be $2,836 for a net of $52,164 and $2,164 more in my pocket. In this case, I am picking the traditional.

A few pro-Roth comments. One year our income was very low. With deductions and child tax credits, we were able to convert about $25,000 from traditional to Roth with $0 taxes paid. Cha-ching! My brother in his early 60s is in a situation where Roth also makes sense. I forget the exact details but it is also true that the Roth is not better until 5 – 10 years in.

Here is the bottom line. When making any decisions about Roth or traditional IRA, please consider your current marginal tax rate and expected average tax rate when you will retire. Sure, it is a guess and requires assumptions, but so does all retirement planning. At least you will be considering the right things.